FM-first — At the Wrong Table, with the Wrong Budget

Getting a seat at the top table is going to take change

ERP modernisation is changing what customers need. It may be the biggest catalyst yet for changing how enterprise perceives iWMS — and the vendors who recognise that and act on it will be the ones who benefit.

Why this matters:

iWMS has always had enterprise-level potential. But it’s been sitting at the wrong table.

FM-first positioning puts iWMS in the room with facilities managers and real estate teams — a smaller room, with a smaller budget, making smaller decisions.

Real estate cost, workplace performance, asset reliability, sustainability data, space utilisation, service quality, operational resilience, and executive decision-making get discussed there too. But in that room, they’re treated as departmental issues. If they were being discussed at the enterprise table, they’d treated as strategic ones — and funded accordingly.

That’s not a branding problem. It’s the difference between a module-sized budget and an enterprise budget, a facilities stakeholder and a CFO, a point solution and a category.

Being at the wrong table has consequences:

- It limits executive access.

- It narrows business-case ambition.

- It constrains deal size.

- It weakens services pull-through.

- It keeps iWMS outside the enterprise transformation conversations where larger budgets, strategic priorities, and long-term operating-model decisions actually get made.

iWMS does not enjoy the enterprise recognition and the associated benefits of other ERP-adjacent technologies like CRM, SCM and HCM.

(see sidebar)

But now there’s an opportunity to change that position, because the current enterprise focus on ERP modernisation and Composable ERP has opened the door to the top table.

Getting a seat there won’t happen automatically. It takes two changes: the market shift already underway with Composable ERP, and a change in how iWMS providers sell.

iWMS providers that make both moves will gain disproportionate mindshare, because no one has claimed the head of this table yet.

Those that don’t will stay exactly where they are — in the smaller room, with the smaller budget, having the smaller conversation.

Why iWMS still struggles for enterprise mindshare

iWMS is a growing enterprise software category but growth does not create strategic status. It still sits well below ERP, CRM, SCM, and HCM in mindshare.

The gap is structural.

No dominant category-defining platform

CRM has Salesforce. HCM has Workday. ERP has SAP and Oracle. iWMS remains fragmented, with no clear gravitational centre that every buyer recognises.

Cost-centre, not revenue framing

CRM is associated with revenue. SCM is associated with continuity and supply-chain risk. iWMS is still associated with facilities and real estate overhead, even though it influences cost, risk, utilisation, sustainability, employee experience, and decision quality.

Legacy perception drag

Parts of the category still carry an on-premise, back-office perception. That weakens the sense that iWMS belongs in the same strategic conversation as cloud ERP, CRM, HCM, data, AI, and enterprise transformation.

Adoption without strategic status

Many organisations have deployed iWMS capabilities, though often in narrow functional areas such as space, maintenance, or facilities operations. But adoption does not automatically create enterprise recognition.

Customers are rethinking ERP strategy

Modern enterprises are shifting toward modular, cloud-based, and AI-enabled architectures that allow faster innovation, lower risk, and better integration with specialized tools.

Their ERP modernisation plans are rejecting legacy monolithic ERP systems like SAP ECC and Oracle E-Business Suite because they are costly, rigid, and slow to adapt to modern business needs.

Customers are not rejecting ERP

ERP remains essential. It runs critical finance, procurement, supply chain, HR, project, contractual, and operational processes. But for many organisations, ERP has become too constraining.

They are rejecting the idea that every business change must depend on the ERP core, the ERP vendor roadmap, a large system integration programme, or the internal IT backlog.

Large ERP environments are expensive to change. Core customisation creates technical debt. Legacy integrations become fragile. Reporting workarounds multiply. Process redesign queues grow. Every new business requirement can become another dependency on the ERP programme.

Vendors like SAP are forcing the rate of modernisation

For SAP customers, the pressure is particularly visible.

SAP says mainstream support for SAP ECC (ERP Central Component) runs until the end of 2027, followed by optional extended maintenance (at a premium cost) until the end of 2030.

That does not mean every ECC customer will migrate to S/4HANA on the same timeline. Some will extend. Some will delay. Some will use third-party support. Some will reassess their ERP roadmap. Some will look for alternative ways to modernise around the core.

But the decision pool is large. (see sidebar)

At the end of 2024, if roughly 14,000 of 35,000 ECC customers had migrated, that implies around 21,000 still faced a migration, extension, replacement, or alternative-support decision. And when you consider that migrations can run between 18 months and 3 years, depending on complexity and customisation, then it’s clear that, for some, it’s already late.

For iWMS providers, these numbers should not be treated as abstract ERP background.

This is a Total Addressable Market with a clock on it.

Thousands of enterprises are being forced to make decisions about core systems, integration, process redesign, data quality, business continuity, user impact, and future operating models.

That is the opening for Composable ERP, and iWMS.

The SAP S4HANA migration backlog is significant

CIO, citing Gartner, reported that at the end of 2024 only 39%, or about 14,000, of SAP’s roughly 35,000 ECC customers had migrated to S/4HANA. Gartner projected that 17,000 ECC customers would still be holdouts by 2027, with 13,000 still on ECC in 2030.

The duration depends heavily on the size of the enterprise, the level of customization in ECC, and the chosen migration approach. Even “fast‑track” migrations rarely finish in under a year.

Many enterprises underestimate the resource demand—SAP specialists, data architects, and change managers are in short supply.

How Composable ERP changes the logic

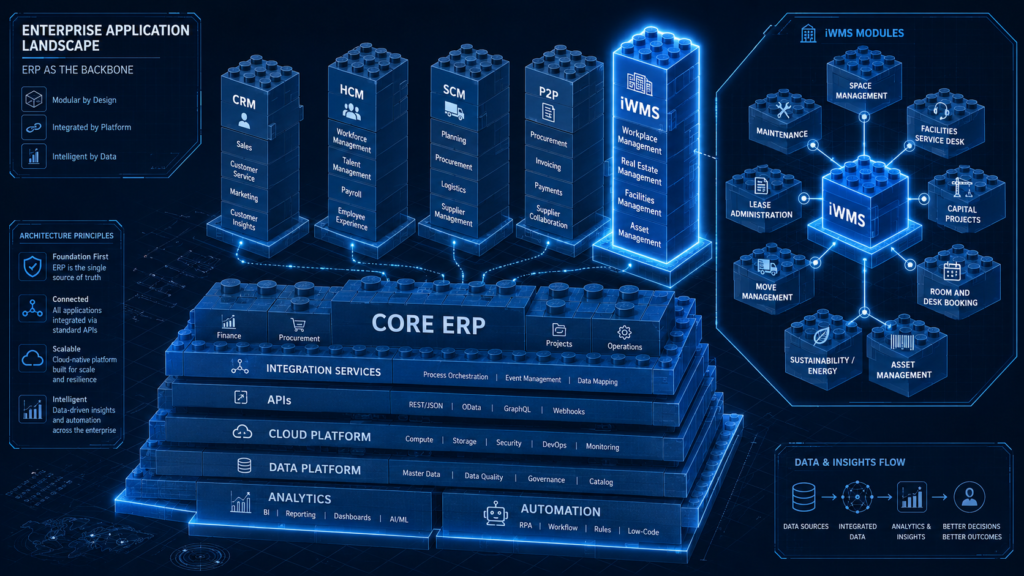

Unlike legacy ERP systems, Composable ERP is not one monolithic system trying to absorb every process. It is a more modular enterprise architecture.

ERP remains the backbone. Around that backbone, customers can use specialist applications, integration services, cloud platforms, APIs, data platforms, analytics, automation, and domain-specific user experiences to support business capabilities that need greater flexibility or deeper domain focus.

In simple terms, the enterprise becomes less like one giant application and more like a governed set of connected capabilities.

SAP’s clean-core strategy points in the same direction. The customer is encouraged to keep the core more standard and upgradeable, while using controlled extensions and adjacent capabilities where differentiation is required.

The practical logic is clear.

The ERP core remains important, but the customer does not have to force every specialist business requirement into that core. Instead, the enterprise can keep the ERP core cleaner, integrate more deliberately, and use specialist solutions where deeper domain capability is needed.

The role of vertical solutions in Composable ERP

That is why vertical solutions matter.

They give customers a way to modernise specialist business capabilities without forcing every workflow, data model, user experience, and operational decision into the ERP core.

The customer benefit of vertical solutions is that they can:

- Provide deeper domain functionality than horizontal ERP

- Faster time to value for specialised business problems

- Less pressure to customise the ERP core

- More relevant user experiences for domain teams

- Clearer ownership of workflows and data

- And a practical bridge between legacy ERP and future ERP.

They may also allow value to be delivered while a larger ERP migration continues, because well-designed vertical solutions can be rolled out alongside SAP, Oracle, or other ERP modernisation programmes. That can soften the impact of legacy systems overhaul by preserving domain continuity, reducing user exposure to core-system disruption, and delivering operational value before the full ERP transformation is complete.

What ERP Can't Manage well — and iWMS Can

The iWMS opportunity is not simply to integrate with ERP.

That is too small and too narrow.

The larger opportunity is to position iWMS as the vertical capability layer for the physical enterprise.

That means the operating layer for real estate, facilities, workplace, space, occupancy, assets, maintenance, service delivery, sustainability, capital planning, risk, and operational performance.

This matters because horizontal ERP is not usually designed to manage the full complexity of the physical enterprise.

ERP can manage finance, procurement, asset records, projects, contracts, and transactions.

But the physical enterprise has its own operating reality: buildings, floors, rooms, equipment, maintenance work, service requests, leases, workplace patterns, employee experience, energy usage, occupancy signals, compliance needs, and local operational constraints.

Those are not minor details. They shape cost, risk, productivity, service quality, employee experience, sustainability performance, and executive decision-making.

A vertical iWMS layer can be better for customers because it provides deeper domain functionality, more relevant user experiences, faster deployment of specific capabilities, clearer ownership of physical-enterprise workflows, and less pressure to customise the ERP core.

The opportunity is not to compete with SAP, Oracle, Microsoft, Infor, or other enterprise platforms. That would be the wrong argument, and it would create unnecessary resistance from ERP vendors, SIs, IT leaders, and enterprise architects.

The stronger message is that iWMS complements ERP.

ERP remains the backbone. iWMS extends enterprise capability into the physical operating environment.

Done well, that’s the shift from the wrong table to the right one — from departmental workflow tool to strategic vertical layer, from operational software to part of the customer’s future enterprise architecture.

That is the category opportunity.

Composable ERP gives iWMS a route into enterprise architecture without claiming to replace ERP. It gives customers a way to modernise physical-enterprise capability without overloading the ERP core.

And it gives iWMS providers the opportunity to gain executive mindshare where the category has often had little visibility.

From cost issues to enterprise value

To earn a seat at the top table, providers need to move beyond feature-led positioning and beyond conventional cost reduction.

High-cost issues do matter. They create urgency. They can get finance attention. They can justify action.

But focusing on high-cost issues will not reposition the category, because if iWMS only sells high-cost issues, it will stay in the cost-centre frame.

The winning play is to connect iWMS to high-value opportunities. That is how iWMS moves from a cost-centre conversation to an enterprise-value conversation.

Composable ERP strengthens that move because it gives iWMS a place in the customer’s future enterprise architecture. The question is no longer:

What cost can this reduce?

The better question is:

What enterprise capability does this create?

That is the question iWMS providers need to answer if they want to move beyond FM-first positioning.

The Composable ERP opportunity is not only a market trend. It has direct implications for vendor leadership.

What this costs if you wait (or is this your High Value Opportunity?)

For the CEO

The issue is category position.

If iWMS continues to be framed as FM-first software, the category remains structurally capped. That affects strategic recognition, enterprise access, ACV potential, services expansion, and long-term account influence.

The uncomfortable point is this: the market has not yet crowned the category-defining iWMS platform.

That is a weakness today, but it is also the opening.

In maturer categories, a vendor trying to reposition the market has to displace a dominant narrative. In iWMS, that narrative is still underdeveloped. The provider that can credibly define iWMS as the enterprise system for the physical operating environment has a chance to shape the category before a dominant position is locked in.

This is a competitive asymmetry.

The first providers to build an enterprise-grade sales motion around Composable ERP may gain mindshare faster than their current market share would suggest.

The question for the CEO is not whether Composable ERP is interesting.

It is whether someone owns the plan to reposition this business before a competitor does — because if no one owns it, the market will decide the answer without you. The category has no incumbent to defend against the first mover.

That means the cost of waiting isn’t neutral. It’s ceding the position permanently to whoever moves first.

For the CRO

The issue is opportunity pipeline and deal economics.

The SAP deadline group represents a large TAM, but that’s not the only one.

The SAP ECC pool is not the only migration statistic. ERP modernisation is underway with most ERP solutions and their customers – Oracle, Microsoft, Infor, and others. For many it is an account universe with a deadline. Not all of those are relevant iWMS prospects. But many are large enterprise accounts already engaged in core-systems, integration, process, data, and operating-model decisions.

These are larger, composite “full stack” solution opportunities.

The current iWMS sales motion often wins module-level budgets from FM or real estate stakeholders. Composable ERP creates a path toward larger enterprise opportunities involving CIO, CFO, COO, transformation, architecture, sustainability, and corporate real estate leadership.

That does not happen through general marketing. It requires account-based targeting, business hypotheses, stakeholder mapping, and a value case tied to the customer’s ERP and enterprise transformation agenda.

The question for the CRO is not whether there is market demand.

It’s whether pipeline is pointed at this account list this quarter — not eventually.

The ECC decision pool has a hard clock on it, and every quarter spent selling module-level budgets to FM buyers is a quarter a competitor spends building the enterprise relationships that will define who wins these accounts when the decision point arrives.

For the CSO

Composable ERP changes the sales conversation. It moves iWMS from FM stakeholders and functional requirements toward CFO/CIO business cases, enterprise architecture, integration governance, transformation risk, and value realisation.

That is a different sale.

The issue is capability.

Many iWMS sales teams are still trained, resourced, and managed for the old one.

They may understand the product. They may understand the modules. They may be able to run a good demo. But ERP-adjacent opportunities require more than product competence.

They require enterprise systems context, diagnostic selling, stakeholder alignment, business-case development, executive engagement, and the ability to connect solution capability to high-cost issues, high-value opportunities, and measurable business outcomes.

The question for the CSO is not whether the sales team needs more messaging.

It’s whether the team can run this conversation today, with the accounts already in motion — or whether by the time they’re ready, those accounts have already been won by someone else’s sales org that retrained first.

The choice now facing iWMS leadership

For years, iWMS has influenced cost, risk, workplace performance, sustainability, asset reliability, service quality, and decision-making — but too often it has still been bought and recognised as “FM” software.

ERP modernisation has created a way to change that: not as another facilities system, but as the vertical capability layer for the physical enterprise.

This will not happen automatically. Customers will not make the connection on their own. ERP teams will not pause their programmes to explain where iWMS fits. CFOs and CIOs will not fund a broader role for iWMS unless the value case is made in language they already use.

That work will get done by somebody. The only open question is whether that work gets done by your organisation — or whether your customers quietly default to their ERP vendor’s own narrow and “safe” FM modules, because no one made the enterprise case for iWMS first.

Composable ERP will not stay an open door. Once ERP vendors’ own native modules become the default answer — because no iWMS provider made the enterprise case before the decision got made — that default hardens fast. It’s far harder to dislodge a bundled incumbent module than to compete against another specialist vendor.

Where this starts

The first step isn’t a strategy offsite — and it isn’t asking sellers to spot these signals on their own. Most aren’t positioned to see them yet; that’s exactly the gap.

We start by identifying accounts that already show these signals — ECC exposure, workplace change, cost pressure — and build the business-opportunity case with sellers. That’s a live, qualified opportunity, not a theoretical one. That’s where ASAP engagement begins.

About ASAP

ASAP is Avvate’s applied sales capability programme for iWMS vendors, integrators, and partners that want to compete more effectively in complex enterprise opportunities.

It is designed for the gap described in this article: the move from product-led, function-level selling to account-based, value-led enterprise engagement.

ASAP helps sales, pre-sales, and leadership teams develop the practical capabilities needed to:

- identify accounts where ERP modernisation, workplace change, cost pressure, sustainability, risk, or operational complexity create a stronger iWMS opportunity;

- develop business opportunity insight before the sales conversation becomes product-led;

- map stakeholders beyond the traditional FM and real estate buyer;

- connect iWMS capability to high-cost issues, high-value opportunities, and executive priorities;

- build stronger value cases and business cases;

- improve confidence in CFO, CIO, COO, transformation, and enterprise-architecture conversations;

- carry the value logic from early engagement into delivery, adoption, and value realisation.

The programme combines structured learning with live opportunity work, so participants are not only learning the approach. They are applying it to real accounts, real stakeholders, and real commercial situations.

The goal is not to turn iWMS sellers into generic consultants.

The goal is to help iWMS teams sell the full enterprise value of the solutions they already provide, with the discipline, confidence, and evidence that larger enterprise opportunities require.